Recent buyers of newly built homes who try to quickly resell their properties may struggle to break even on what they paid, raising a warning for buyers who aren’t planning to remain in their homes long term.

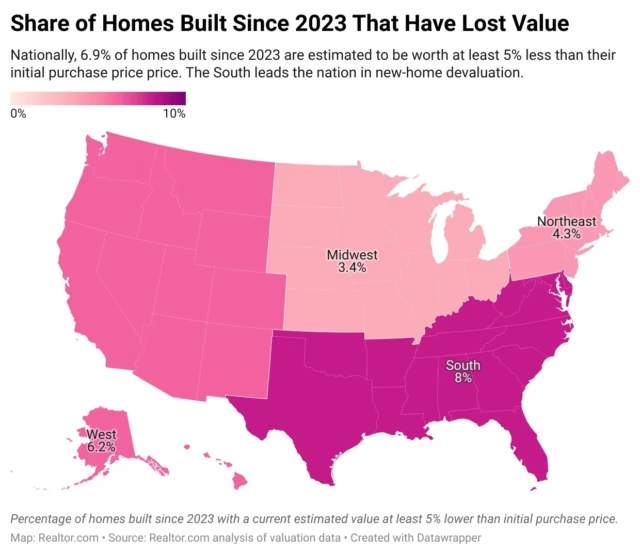

Nationally, 6.9% of all homes constructed since 2023 are worth at least 5% less than their initial purchase price, according to a Realtor.com® analysis of property value estimates. The problem is the worst in the South, where 8% of new homes are valued substantially below their initial purchase price.

The trend follows a steady series of price cuts from homebuilders, which can weaken the resale value of similar properties nearby. As well, builders in recent years have relied heavily on incentives such as mortgage rate buydowns, allowing them to command higher prices than they might otherwise.

As a result, sellers of newly built homes who purchased since 2023 are more than twice as likely to resell their home at a loss than are sellers of existing homes who bought and sold in the same period, according to Realtor.com senior economist Joel Berner.

“We know from previous research that new-home buyers have recently been getting significantly lower mortgage rates than existing-home buyers,” says Berner. “This may come in exchange for paying a slightly higher price for the home.”

The problem is far from ubiquitous: Most newly built homes are still holding their value or appreciating, and most homebuyers don’t try to sell their property just one or two years after a purchase.

However, the trend raises a warning flag for homebuyers who are considering a new-construction purchase and feel that job changes or life circumstances could force them to sell again in a few years.

“If their home value were to fall, they could find themselves in a position where they owe more on their home than it’s worth, or they’re ‘upside-down,'” says Berner. “When they then go to sell their home, they may not have enough proceeds to cover the balance on their mortgage.”

Mortgage rate buydowns: The incentive with strings attached

For several years, major homebuilders have been offering deep discounts on in-house mortgage rates to stimulate demand and work through a glut of unsold inventory.

In the third quarter of 2025, the average 30-year mortgage rate for new-construction homes sold in the period was 5.27%, nearly a full percentage point lower than for existing homes, according to recent Realtor.com research.

On the typically priced new home with 10% down, that rate discount would lower monthly payments by more than $230 per month, potentially bringing an otherwise unaffordable home into reach for the buyer.

But the bargain rates offered by homebuilders are typically not transferable, meaning that when the home is offered for resale, it must appeal to prospective buyers who have to budget for market-rate mortgages.

At current home prices, the purchase price would have to drop by about 10% to achieve the same monthly payment savings seen with a 1% decrease in mortgage rates.

That disconnect may leave quick resellers of new homes at a disadvantage when they list, especially if similar home models are still available from the homebuilder with rate discounts or other incentives.

And there is emerging evidence that new-home buyers who take advantage of builder mortgage discounts are more likely to end up underwater, as recently reported in The Wall Street Journal.

John Comiskey, founder of Reverse Engineering Finance, recently analyzed FHA mortgage data and found that the lender arms of major homebuilders had some of the highest percentages of underwater mortgages for loans originated in 2022 through 2024.

Lennar’s mortgage arm tops the list, with 27% of loans originated in that period now underwater, according to Comiskey. The lending arm of D.R. Horton, the nation’s biggest builder, comes in at 18%.

Those stats compare unfavorably with Quicken Loans, a broad-based lender with similar origination volume, which had just 10% of recently issued loans underwater.

“To avoid this scenario, new-home shoppers should be sure to negotiate a competitive price for the home independent of whatever incentives the builder may be offering,” says Berner. “Low rates are great, but don’t accept them as a substitute for the right purchase price.”

realtor.com

DECEMBER 23, 2025