When Amanda and Vincent DeRise went to view a 140-year-old Victorian home for sale in Atlantic Highlands, NJ, their real estate agent didn’t mince words: It was a “money pit.”

But the DeRises saw a way into the wealth engine that has defined middle-class America for generations.

While it’s no secret that homeownership builds wealth through equity and appreciation, new research from Realtor.com® reveals a critical factor: timing.

At 31 and 32, the DeRises were in a race against the clock to lock in home equity gains that could net them a 22.5% higher net worth by the age of 50—the equivalent of $119,000—than if they had waited to buy in their 40s.

“This data really does show that buying a home can be an accelerator for your net worth,” explains Hannah Jones, Realtor.com senior economic research analyst and author of the report.

But today, that early-buyer edge is running headlong into high costs in a highly competitive landscape that’s edging out younger house hunters.

That’s what led the DeRises to the century-old fixer-upper. After touring homes that needed less work, Vincent says they quickly realized the market was tilted toward cash and speed.

Amanda and Vincent DeRise in front of their 140-year-old “money pit.”PHOTO COURTESY OF AMANDA AND VINCENT DERISE.

Amanda and Vincent DeRise in front of their 140-year-old “money pit.”PHOTO COURTESY OF AMANDA AND VINCENT DERISE.“We were getting beat out by contractors and folks that were offering cash, or offering like $100,000 over asking price,” he says.

That tension—between the wealth boost of buying early and the shrinking ability to do it—now sits at the center of the American housing story.

In a series of new interviews, Realtor.com has spoken to families across the country who describe what it takes to get a foot in the door, what happens when they can’t, and the ripple effect of those gaps across generations.

Why ‘buying early’ is disappearing

In 1990, the typical American bought their first home at age 30. By 2026, the median age of the first-time buyer is 40, according to research from the National Association of Realtors®.

It’s a challenge that Jackie Lam, a freelance writer and an accredited financial counselor who rents outside Pasadena, CA, knows well.

Jackie Lam says the 2025 Los Angeles wildfires solidified her decision to exit the homebuying market.PHOTO COURTESY OF JACKIE LAM.

Jackie Lam says the 2025 Los Angeles wildfires solidified her decision to exit the homebuying market.PHOTO COURTESY OF JACKIE LAM.Lam has been a renter her entire adult life. Despite getting pre-approved for a mortgage a few years ago, she found the market nearly impenetrable.

“It’s just really, really hard,” she says, noting that her options were limited to small condos—a far cry from the three-bedroom starter homes of previous generations.

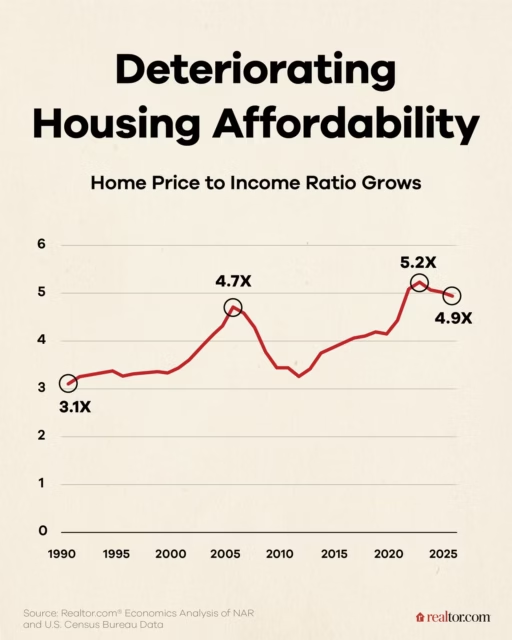

The ratio of home prices to incomes today helps explain that squeeze.

In 1990, the median home price was $96,800 and the median household income was $31,000—a price-to-income ratio of about 3.1, according to a Realtor.com analysis of NAR and U.S. Census Bureau data. Today, the median home price is $418,000 and the median household income is $85,000—pushing that ratio to 4.9.

With a higher threshold to entry, it’s harder for younger buyers to break through. While the DeRises managed to buck the trend, they did so only by purchasing a house that needed major work.

“We were really naive. A lot of money, a lot of time, a lot of sacrifices,” says Vincent of their choice.

The DeRises say they were “really naive” in purchasing a home that needed so much work.PHOTO COURTESY OF AMANDA AND VINCENT DERISE.

The DeRises have self-funded their renovations with savings and a 401(k) loan.PHOTO COURTESY OF AMANDA AND VINCENT DERISE.

“We’ve sacrificed so much,” says Vincent of their choice to invest in their home instead of a honeymoon, vacations, and nights out with friends.PHOTO COURTESY OF AMANDA AND VINCENT DERISE

Since closing on their home in October 2024 for $550,000, they’ve put $175,000 into renovations—all self-funded and not including the cost of months of decision fatigue, disrupted routines, and the constant thrum of construction.

Realtor.com

MARCH 12, 2026