America is minting millionaires at a remarkable pace—but for many households, that wealth exists more on paper than in the bank.

As home prices surged, many homeowners were pushed closer to seven-figure net worth through rising equity. But the same market that helped create those millionaire balance sheets has also made it harder, slower, and more expensive for the next generation to buy in at all.

Today, more than 24 million U.S. households have a net worth above $1 million, according to a Bloomberg analysis of Federal Reserve data, and one-third of those millionaire households have been minted since 2017.

That tracks closely with housing: From 2017 to 2023, the national median home price rose 35%, and by 2025, a simple starter home cost $1 million or more in more than half of all states, according to data from Realtor.com®.

“Millionaire status is closely tied to homeownership and resultant home equity,” explains Joel Berner, senior economist at Realtor.com. “Building home equity is the mechanism by which those accumulating wealth can put away some of their income each month and see that money grow with the value of their home.”

But as the typical age for a first-time homebuyer stretches to 40, it poses a complication: More Americans may be reaching millionaire status through housing, even as fewer have the runway to build that kind of wealth themselves.

How housing has made so many millionaires

So why is owning a home such a wealth builder?

The Urban Institute describes homeownership as the anchor of long-term wealth accumulation in a recent report.

Once households get into ownership, the wealth effect compounds. The report found that median home equity rises from about $180,000 within the first five years after purchase to more than $340,000 by years six through 10, then continues climbing with longer tenure.

That helps explain why so many households can cross the seven-figure net-worth threshold without looking or feeling especially affluent—they just keep living in the same house, and over time, their equity stake in that house can swell.

It also helps explain why the old idea of the “millionaire next door” may be even more relevant today than when it was first popularized in 1996 by the bestselling book of the same name.

The book challenged the image of a millionaire as someone who struck it rich in stocks or business, instead portraying millionaires as ordinary-looking households (like your neighbors) whose wealth was real but understated—people who spent carefully and built net worth steadily over time.

It’s what Realtor.com Chief Economist Danielle Hale calls the “get rich slow scheme” of homeownership, and Berner says that’s exactly the dynamic playing out for many millionaires today.

“These figures suggest that those who become millionaires do so with high-growth investments rather than simply piling up cash, and that most of them own homes rather than rent,” he says. “These are long-term approaches to wealth building, so these newly minted millionaires may not have major positive cash flows during their years of working, saving, and building up home equity.”

But Berner adds there are other sneaky ways that homeownership can build wealth.

“We showed that homeownership correlates with higher rates of saving, even on top of home equity building,” he says, pointing to recent research from Realtor.com on generational wealth and homeownership. “This level of financial acumen and discipline leads some to become millionaires and others to be left behind.”

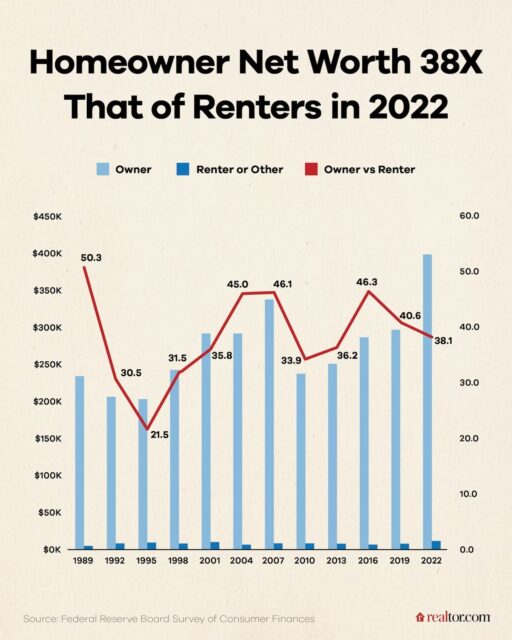

Over time, that combination can produce a very large balance-sheet effect. Homeowners’ median net worth has typically been 30 to 50 times that of renters since 1989, according to a Realtor.com analysis of Federal Reserve Survey of Consumer Finances data.

It’s a clear illustration of why homeownership remains one of the clearest paths to millionaire status. It also offers an important reframing of homeownership today: While high prices have recast homeownership as the end goal of wealth creation, the data instead points to it as where real wealth creation begins.

Realtor.com

APRIL 14, 2026